JPMorgan European Discovery Trust JEDT share price, company news, analysis and interviews

JPMorgan European Discovery Trust plc (LON:JEDT) aims to provide capital growth from a diversified portfolio of smaller European companies (excluding the United Kingdom). As the emphasis is on capital growth rather than income, shareholders should expect the dividend to vary from year to year. The investment trust JEDT has the ability to use borrowing to gear the portfolio within the range of 20% net cash to 20% geared, in normal market conditions.

In the video below JP Morgan European Discovery Trust plc Francesco Conte presents a review at the AGM in July 2023. The video contains a detailed review of the investment performance of the trust, a summary of investment approach and recent activity and outlook.

JPMorgan European Discovery Trust plc considers financially material Environmental, Social and Governance (ESG) factors in investment analysis and investment decisions, with the goal of enhancing long-term, risk-adjusted financial returns.

Important Announcement

With effect from 15 June 2021, and update of the ticker on 17 June 2021, the name and ticker of the Company have changed to JPMorgan European Discovery Trust plc (JEDT from JESC). These changes better reflect the Company’s investment strategy and its portfolio. Some of the Company’s portfolio companies have market capitalisations of up to EUR8bn; as such the Board believes that the Company’s name did not accurately describe the portfolio holdings or the investment opportunities available to the Investment Managers. All other Company details remain the same, including the Company’s ISIN, SEDOL and LEI.

Share this page

Twitter

LinkedIn

Facebook

Email

WhatsApp

JPMorgan European Discovery Trust JEDT share price

Discover the growth potential of European equities with JPMorgan European Discovery Trust plc (LON:JEDT). Investing in smaller companies across Europe for capital growth.

Explore UK investment trusts as an ideal option for your stocks and shares ISA. Discover opportunities in Japan, Emerging Markets, European small caps, UK, Energy, and Latin America for tax-free growth.

JPMorgan European Discovery Trust plc (LON:JEDT) has announced its January commentary.

JEDT’s share price and NAV rose 19.03% and 15.05% respectively on a cumulative basis to 31 January 2024

Month in review – As of 31/01/2024

The trust outperformed its benchmark over January.

Positive contributors to relative returns included stock selection in industrial engineering and stock selection and an overweight position in industrial support services.

Detractors included stock selection and an underweight position in industrial transportation and stock selection in technology hardware and equipment.

At the stock level, an overweight position in Kindred, a Swedish gambling company, outperformed after receiving a takeover offer from Francaise des Jeux.

An overweight position in SPIE, a French multi-technical services company, outperformed as the company continued to benefit from strong investments into electrification & energy efficiency.

Conversely, an overweight position in Forvia, a French auto parts supplier, underperformed as concerns emerged around their ability to pass on price increases while demand for autos seems to be slowing.

An overweight position in Melexis, a Belgian automotive chip designer, also underperformed as the inventories of chips have started to increase at auto original equipment manufacturers (OEMs), signaling a potential slowdown in demand.

Looking ahead – As of 31/01/2024

On top of the macroeconomic uncertainties, there are numerous political uncertainties arising out of the ongoing geopolitical tensions and the imminent national elections.

European equities trade on an extreme discount to US equities, a discount that has grown following strong 2023 technology-led gains in the US. This argument may not be new to prospective investors; however, the European equity market today can offer comparable levels of quality and growth potential.

While the short-term outlook remains uncertain, we believe European equities offer an attractive entry point to the long-term investor, and we remain focused on selecting companies with pricing power, strong balance sheets and the ability to grow significantly over the long term.

JPMorgan European Discovery Trust plc (LON:JEDT) is an investment trust company. The Investment Trust JEDT objective is to achieve capital growth from a portfolio of quoted smaller companies in Europe, excluding the United Kingdom.

JPMorgan European Discovery Trust plc (LON:JEDT) appoints new Portfolio Managers, bringing extensive experience and outperformance records to the company.

JP Morgan European Discovery Trust plc (LON:JEDT) Co-Portfolio Manager and Managing Director, Francesco Conte presents a review of the European investment trust at the AGM in July 2023. The video contains a detailed review of the investment performance of the trust, a summary of investment approach and recent activity and outlook.

https://vimeo.com/891113352

JPMorgan European Discovery Trust plc (LON:JEDT) is an investment trust company. The Investment Trust JEDT objective is to achieve capital growth from a portfolio of quoted smaller companies in Europe, excluding the United Kingdom.

JPMorgan European Discovery Trust plc (LON:JEDT) Portfolio managers Francesco Conte and Edward Greaves discuss what makes European stocks attractive right now and how they uncover hidden gems before they are discovered by the wider investing community.

DirectorsTalk interviewed Edward Greaves, Portfolio Manager for JPMorgan European Discovery Trust plc (LON: JEDT) to discuss the investment case for European smaller companies, current valuations in the sector as well as long-term themes within the portfolio for this Europe investment fund.

Q1. Edward, why should investors look at European smaller companies now?

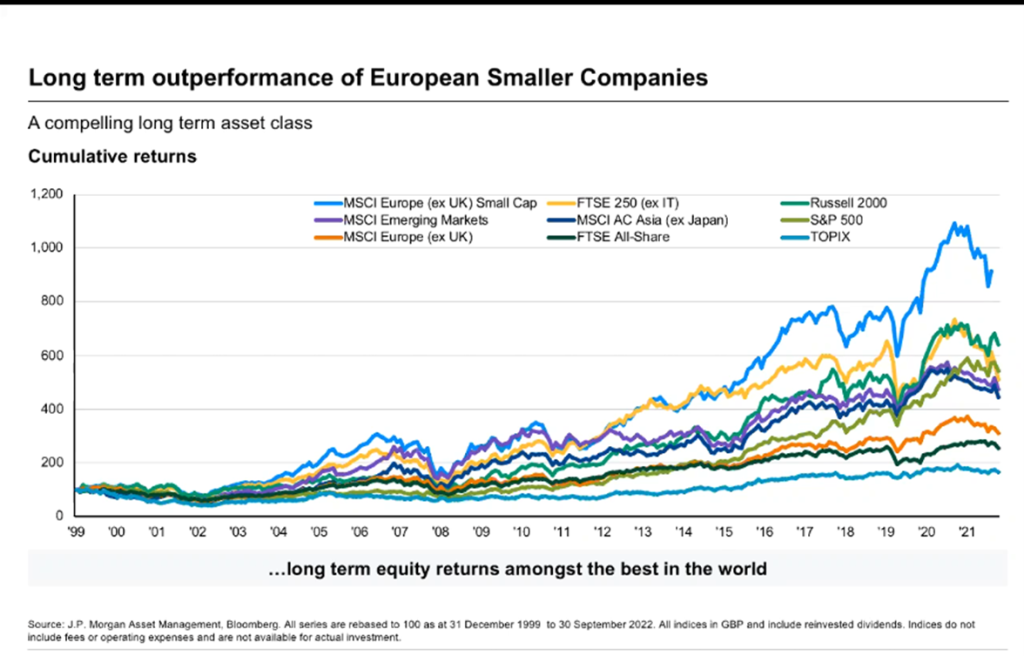

Well, in my view, we mustn’t lose track of the bigger picture, we shouldn’t forget that European small caps have been one of the best performing asset classes for decades and this surprises many people.

This chart shows the long term performance of the investment trust’s benchmark versus a number of global equity indices since 2000. The benchmark is in blue and you can see that it has outperformed all of the other major indices over this period and we show reinvested dividends in pound sterling.

This is due to the superior growth of European small caps. Small caps are more entrepreneurial, more dynamic, they’re more nimble, they’re able to very quickly recognise and exploit new themes or trends.

At the same time, current valuations are very attractive. The price to book ratio of our benchmark is really low – it’s approaching the levels seen at the peak of the global financial crisis and the Eurozone sovereign debt crisis. This is similar when you look at the price to book ratio of European small caps versus large caps.

Q2. Can you put the performance of European small caps in a historical context?

The evidence shows small caps tend to underperform during a global crisis and this is when risk premiums increase. At this point, central banks step in to support the economy and small caps stage rapid recoveries. This whole process was very much accelerated through COVID-19 when central banks stepped in really quickly and small caps actually outperformed for the year.

Year-to-date, small caps have underperformed[1] significantly versus large caps but at the same time, forward economic indicators are now very very poor, approaching levels where central banks have stepped up support historically.

As soon as sentiment turns more positive, I would expect that small caps would stage a very good rally especially given the long-term outperformance of the asset class and the depressed valuations that we see currently.

Q3. Can you remind investors of the investment trust’s investment process.

Of course. We look to uncover hidden gems before the wider investing community does and many of the small caps that we have invested in have gone on to become large caps or have been acquired by larger companies.

Our investment strategy focusses on three characteristics: value, quality and momentum. So, just to take each of these in turn.

Value – We really focus on free cash flow yield because we believe this is the highest quality valuation metric. We think cash is king, cash is needed for investments and cash is needed for dividends. We look for earnings recovery potential so for example, catalysts and we want some intrinsic quality, we don’t want to be investing in price taking commodities as these often turn out to be value traps.

Quality – We want companies that are market leaders in niches, we want high pricing power, low capex requirements so in other words, high return on invested capital. We’re looking for very strong balance sheets and importantly, we want management teams with proven track records and efficient capital allocation. We meet hundreds of companies every year and the CEO’s/CFO’s are often the company founders themselves and this gives us a clearer understanding of their capital allocation decision process and management tools. We believe this is an extremely important part of the investment process.

Momentum – We’re looking for companies where we see future earnings potential not reflected in expectations. This could be due to the structural growth of the end markets for example, aging populations, it could be that the company has a disruptive technology that’s gaining market share or it could be companies that operate in fragmented markets and have a track record of successful bolt-on acquisitions, this allows them to consolidate the market.

Importantly, it’s difficult to find companies that look great for all three characteristics so we look for companies that score well for at least two of these and we ensure that the overall portfolio is bias towards all three of them, this ensures we have a balanced portfolio. We’ve got both very exciting growth companies and we’ve got attractively valued companies with strong earnings recovery potential.

Can you highlight some of the themes that emerge from your investment strategy?

We have a big exposure to renewable energy, electrification, and environmental protection via companies such as:

Spie, which is an installation company heavily exposed to the energy transition theme,

Erg, which is a renewable energy generation company,

Nexans, which is a global leader in high voltage cables which are vital to connecting renewable energy to the grid and upgrading the grid itself to cope with more volatile supply and demand,

Arcadis, which is an engineering consultant focussed on buildings, infrastructure, environment, and water.

We also have exposure to leisure activities after COVID lockdowns have ended via companies such as Kinepolis which is an exceptionally well run cinema chain and importantly, has a very strong balance sheet.

We have many companies exposed to technological disruption such as:

Melexis which is a beneficiary of every-growing semi-conductor content for cars, and this should support continued double-digit growth going forward,

Reply is an IT consultant focussed on themes such as big data, artificial intelligence and cyber security which all companies have to invest in, regardless of the sector they operate in,

Medtech diagnostics company, DiaSorin, which is benefitting from aging populations and the growing importance of diagnostics testing.

From this, you can see another benefit of small cap investing which is the ability to get pure exposure to many different, exciting, new growth themes.

So, just to summarise, whilst the short term economic outlook is very uncertain, we like to focus on the fact that European small caps as an asset class has a great long-term track record, it’s very cheap versus history and this trust has a very experience management team and a disciplined investment process.

JPMorgan European Discovery Trust plc (LON:JEDT) aims to provide capital growth from a diversified portfolio of smaller European companies (excluding the United Kingdom).

Investment objectives: The Company aims to provide capital growth from a diversified portfolio of smaller European companies (excluding the United Kingdom). As the emphasis is on capital growth rather than income, shareholders should expect the dividend to vary from year to year. The Company has the ability to use borrowing to gear the portfolio within the range of 20% net cash to 20% geared, in normal market conditions.

Key Risks: Exchange rate changes may cause the value of underlying overseas investments to go down as well as up. External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions. This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down. This Company invests in smaller companies which may increase its risk profile. The share price may trade at a discount to the Net Asset Value of the Company.

Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

[1] Source: J.P. Morgan Asset Management, Bloomberg. As of September 2022. Before 2022, the comparison was between EMIX smaller European Companies (ex UK) Index vs. MSCI Europe (ex UK) Index, and since then, MSCI Europe Small Cap (ex UK) Index vs MSCI Europe (ex UK) Index. All indices in GBP and include reinvested dividends. Indices do not include fees or operating expenses and are not available for actual investment. The indices used are based on data availability and changes to internal system’s data source.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained free of charge in English from JPMorgan Funds Limited or at www.jpmam.co.uk/investmenttrust.

This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

Past performance is not a reliable indicator of current and future results.

JPMorgan European Discovery Trust plc (LON:JEDT) Portfolio managers Francesco Conte and Edward Greaves discuss what makes European stocks attractive right now and how they uncover hidden gems before they are discovered by the wider investing community.

DirectorsTalk interviewed Edward Greaves, Portfolio Manager for JPMorgan European Discovery Trust plc (LON: JEDT) to discuss the investment case for European smaller companies, current valuations in the sector as well as long-term themes within the portfolio for this Europe investment fund.

Q1. Edward, why should investors look at European smaller companies now?

Well, in my view, we mustn’t lose track of the bigger picture, we shouldn’t forget that European small caps have been one of the best performing asset classes for decades and this surprises many people.

This chart shows the long term performance of the investment trust’s benchmark versus a number of global equity indices since 2000. The benchmark is in blue and you can see that it has outperformed all of the other major indices over this period and we show reinvested dividends in pound sterling.

This is due to the superior growth of European small caps. Small caps are more entrepreneurial, more dynamic, they’re more nimble, they’re able to very quickly recognise and exploit new themes or trends.

At the same time, current valuations are very attractive. The price to book ratio of our benchmark is really low – it’s approaching the levels seen at the peak of the global financial crisis and the Eurozone sovereign debt crisis. This is similar when you look at the price to book ratio of European small caps versus large caps.

Q2. Can you put the performance of European small caps in a historical context?

The evidence shows small caps tend to underperform during a global crisis and this is when risk premiums increase. At this point, central banks step in to support the economy and small caps stage rapid recoveries. This whole process was very much accelerated through COVID-19 when central banks stepped in really quickly and small caps actually outperformed for the year.

Year-to-date, small caps have underperformed[1] significantly versus large caps but at the same time, forward economic indicators are now very very poor, approaching levels where central banks have stepped up support historically.

As soon as sentiment turns more positive, I would expect that small caps would stage a very good rally especially given the long-term outperformance of the asset class and the depressed valuations that we see currently.

Q3. Can you remind investors of the investment trust’s investment process.

Of course. We look to uncover hidden gems before the wider investing community does and many of the small caps that we have invested in have gone on to become large caps or have been acquired by larger companies.

Our investment strategy focusses on three characteristics: value, quality and momentum. So, just to take each of these in turn.

Value – We really focus on free cash flow yield because we believe this is the highest quality valuation metric. We think cash is king, cash is needed for investments and cash is needed for dividends. We look for earnings recovery potential so for example, catalysts and we want some intrinsic quality, we don’t want to be investing in price taking commodities as these often turn out to be value traps.

Quality – We want companies that are market leaders in niches, we want high pricing power, low capex requirements so in other words, high return on invested capital. We’re looking for very strong balance sheets and importantly, we want management teams with proven track records and efficient capital allocation. We meet hundreds of companies every year and the CEO’s/CFO’s are often the company founders themselves and this gives us a clearer understanding of their capital allocation decision process and management tools. We believe this is an extremely important part of the investment process.

Momentum – We’re looking for companies where we see future earnings potential not reflected in expectations. This could be due to the structural growth of the end markets for example, aging populations, it could be that the company has a disruptive technology that’s gaining market share or it could be companies that operate in fragmented markets and have a track record of successful bolt-on acquisitions, this allows them to consolidate the market.

Importantly, it’s difficult to find companies that look great for all three characteristics so we look for companies that score well for at least two of these and we ensure that the overall portfolio is bias towards all three of them, this ensures we have a balanced portfolio. We’ve got both very exciting growth companies and we’ve got attractively valued companies with strong earnings recovery potential.

Can you highlight some of the themes that emerge from your investment strategy?

We have a big exposure to renewable energy, electrification, and environmental protection via companies such as:

Spie, which is an installation company heavily exposed to the energy transition theme,

Erg, which is a renewable energy generation company,

Nexans, which is a global leader in high voltage cables which are vital to connecting renewable energy to the grid and upgrading the grid itself to cope with more volatile supply and demand,

Arcadis, which is an engineering consultant focussed on buildings, infrastructure, environment, and water.

We also have exposure to leisure activities after COVID lockdowns have ended via companies such as Kinepolis which is an exceptionally well run cinema chain and importantly, has a very strong balance sheet.

We have many companies exposed to technological disruption such as:

Melexis which is a beneficiary of every-growing semi-conductor content for cars, and this should support continued double-digit growth going forward,

Reply is an IT consultant focussed on themes such as big data, artificial intelligence and cyber security which all companies have to invest in, regardless of the sector they operate in,

Medtech diagnostics company, DiaSorin, which is benefitting from aging populations and the growing importance of diagnostics testing.

From this, you can see another benefit of small cap investing which is the ability to get pure exposure to many different, exciting, new growth themes.

So, just to summarise, whilst the short term economic outlook is very uncertain, we like to focus on the fact that European small caps as an asset class has a great long-term track record, it’s very cheap versus history and this trust has a very experience management team and a disciplined investment process.

JPMorgan European Discovery Trust plc (LON:JEDT) aims to provide capital growth from a diversified portfolio of smaller European companies (excluding the United Kingdom).

Investment objectives: The Company aims to provide capital growth from a diversified portfolio of smaller European companies (excluding the United Kingdom). As the emphasis is on capital growth rather than income, shareholders should expect the dividend to vary from year to year. The Company has the ability to use borrowing to gear the portfolio within the range of 20% net cash to 20% geared, in normal market conditions.

Key Risks: Exchange rate changes may cause the value of underlying overseas investments to go down as well as up. External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions. This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down. This Company invests in smaller companies which may increase its risk profile. The share price may trade at a discount to the Net Asset Value of the Company.

Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

[1] Source: J.P. Morgan Asset Management, Bloomberg. As of September 2022. Before 2022, the comparison was between EMIX smaller European Companies (ex UK) Index vs. MSCI Europe (ex UK) Index, and since then, MSCI Europe Small Cap (ex UK) Index vs MSCI Europe (ex UK) Index. All indices in GBP and include reinvested dividends. Indices do not include fees or operating expenses and are not available for actual investment. The indices used are based on data availability and changes to internal system’s data source.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained free of charge in English from JPMorgan Funds Limited or at www.jpmam.co.uk/investmenttrust.

This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

Past performance is not a reliable indicator of current and future results.

JPMorgan European Discovery Trust JEDT share price

Fundamentals

Share this page

Twitter

LinkedIn

Facebook

Email

WhatsApp

Data policy – All information should be used for indicative purposes only. You should independently check data before making any investment decision and or seek professional advice. DirectorsTalk cannot guarantee that the data is accurate or complete, and accepts no responsibility for how it may be used.