Cadence Minerals plc (NEX LON:KDNC; OTC: KDNCY) has announced the completion of the Pre-Feasibility Study on the Amapá Iron Ore Project, Brazil.

The PFS confirms the potential for the Amapá Iron Ore Project to produce a high-grade iron ore concentrate and generate strong returns over its life of mine. Completing the PFS is a significant milestone in the Project’s development, laying the foundations to advance Amapá to eventual production.

Cadence holds a 30% interest in Pedra Branca and, consequently, a 30% interest in the Amapá Project and has a first right of refusal to increase its interest to 49%.

The PFS was managed by Pedra Branca Alliance Pte. Ltd., Cadence and Indo Sino Pte. Ltd. and has been compiled by Wardell Armstrong International. WAI is a leading, globally recognised mining consultancy with a track record of conducting all levels of technical study required on projects that have successfully been financed and developed into mining operations.

PFS Highlights:

- Annual average production after ramp-up of 5.28 million dry metric tonnes per annum (“Mtpa”) of Fe concentrate, consisting of 4.36 Mtpa at 65.4% Fe and 0.92 Mtpa at 62% Fe concentrate.

- Post-tax Net Present Value (“NPV”) of US$949 million (“M”) at a discount rate of 10%, with profit after tax of US$2.96 billion (“B”) over Life of Mine (“LOM”) gross revenues of US$9.39 B over LOM.

- Post-tax Internal Rate of Return of 34%, with an average annual LOM EBITDA of US$235 M per annum.

- Maiden Ore Reserve of 195.8 million tonnes (“Mt”) at 39.34% Fe, demonstrating an 85% mineral resource conversion.

- Free on Board (“FOB”) C1 Cash Costs of US$35.53/dmt at the port of Santana. Cost and Freight (“CFR”) C1 Cash Costs US$64.23/dmt in China.

- After applying tax rebates, a pre-production capital cost estimate of US$399 M, including the improvement and rehabilitation of the processing facility and the restoration of the railway and the wholly owned port export facility, cost estimations have a PFS level of accuracy at +/- 25%.

- Key assumptions: Long-term average price for 62% iron ore concentrate of US$95/dmt and US$23.8/dmt premium for 65.4% iron ore concentrate, both quoted on a Cost and Freight (“CFR”) basis.

- Opportunities: exploration target at the Tucano Mine to further extend initial mine life and potential capital savings at port loading facilities.

Based on the positive outcome of the PFS, the owner of the Project DEV Mineração S/A (“DEV”) intends to advance the Project. The initial works will include optimising the capital expenditure, optimising processing plant availability and efficiency and developing the adjacent exploration targets to increase the mine life, after which work on a Feasibility Study can begin.

Cadence CEO Kiran Morzaria commented: “On behalf of the Cadence Board, we are pleased and proud to release the Pre-Feasibility Study for the Amapá Iron Ore Project in Brazil. This study, which we consider to be a definitive moment for our company, re-enforces Cadence’s analysis that the Amapá Project can be regenerated and restarted on a profitable basis over an initial 16-year mine life.”

“The Study outlines a robust 5.28 Mtpa operation which can deliver excellent cash flows, and a post-tax NPV of US$949 million producing 4.36 Mtpa of 65.4% iron ore concentrate and 0.92 Mtpa of 62% iron ore concentrate.”

“We are also pleased to declare a maiden Ore Reserve of 195.8Mt at 39.34%, representing 85% resource to reserve conversion and confirming the robust project fundamentals.”

“The Project benefits from integrated infrastructure under the owner’s control, a well-established processing route, low capital intensity and a quality product with an international reputation. Along with a skilled workforce, proximity to operational infrastructure and the potential to increase the mineral resource means that Amapá remains an incredibly attractive investment opportunity.”

“The opportunity for DEV is to advance the Amapá Iron Ore Project to a Financial Investment Decision. This could be completed along with securing a strategic investor, offtake partner, separate listing, or a combination of these options. However, we recognise that there is still much work to complete at Amapá, which will ultimately deliver a Feasibility Study.”

“I look forward to reporting further progress across all our projects in the coming months.”

Table 1.1 Key Project Metrics (100% project basis)

| Metric | Unit | 2022 PFS Data |

| Total ore feed to the plant | Mt (dry) | 176.88 |

| Life of Mine | Years | 16 |

| Fe grade of ore feed to the plant | % | 39.34 |

| Recovery | % | 76.27 |

| 62.0% iron ore concentrate production | Mtpa | 0.89 |

| 65.4% iron ore concentrate production | Mtpa | 4.23 |

| C1 Cash Costs FOB * | US$/dmt | 35.53 |

| C1 Cash Costs CFR ** | US$/dmt | 64.23 |

| Pre-Production capital investment*** | US$M | 399 |

| Sustaining capital investment over LOM**** | US$M | 245 |

| Post-tax NPV (10%) | US$M | 949 |

| Post-tax IRR | % | 34 |

| Project payback | Years | 4 |

| Total profit after tax (net operating profit) | US$B | 2.96 |

| * | Means operating cash costs, including mining, processing, geology, OHSE, rail, port and site G&A, divided by the tonnes of iron ore concentrate produced. It excludes royalties and is quoted on a FOB basis (excluding shipping to the customer). |

| ** | Means the same as C1 Cash Costs FOB; however, it includes shipping to the customer in China (CFR). |

| *** | Includes direct tax credit rebate over 48 months |

| **** | Includes both sustaining CAPEX and deferred capital expenditure, specifically, improvements to the railway and the installation of conveyor belt and mine site to rail load out |

Summary of Amapá Iron Ore Project PFS Results

The information in the press release contains a summary of the PFS and its results

Introduction

The Project consists of an open-pit iron ore mine, a processing and beneficiation plant, a railway line, and an export port terminal. DEV and its subsidiaries own the Amapá Project. DEV is owned by PBA, a joint venture between Cadence Minerals Plc and Indo Sino Trade Pte Ltd.

The Project ceased operations in 2014 after the port facility suffered a geotechnical failure, which limited the export of iron ore. Before the cessation of operations, the Project generated an underlying profit of US$54 million in 2012 and US$120 million in 2011[1]. Operations commenced in December 2007, and in 2008, the Project produced 712 thousand tonnes of iron ore concentrate. Production steadily increased, producing 4.8 Mt and 6.1 Mt of iron ore concentrate products in 2011 and 2012, respectively.

DEV continued to operate the Project and rehabilitate the port up until 2014. However, due to the restricted iron ore exports, and cash flow constraints, in August 2015, DEV filed for judicial protection in Brazil, and operations at the Project ceased.

In 2019 Cadence and Indo Sino, alongside DEV, submitted a judicial restructuring plan (“JRP”) for approval by the unsecured creditors. As part of the JRP, DEV sought to redevelop the Amapá Project. This strategy includes a plan to resume operations after plant revitalisation and modifications, aimed at improving product quality and increasing recovery, along with recovery of the port, railway, and support areas.

It should be noted that the Amapá Project, and Pre-Feasibility Study (“PFS”), has been managed by Indo Sino and Cadence in co-operation with Wardell Armstrong International (“WAI”); the latter has reviewed the work completed and compiled the PFS. The PFS and supporting reports, engineering designs and data are the sole property of PBA.

The Mineral Resource and Ore Reserve statements have been prepared in accordance with the Guidelines of the Australasian Code for Reporting of Exploration Results, Mineral Resources, and Ore Reserves, the JORC Code, 2012 Edition (JORC Code (2012)). Cost estimations were prepared by DEV, with input from third-party independent engineers and subsequently reviewed by WAI using the internationally accepted practice for PFS-level studies.

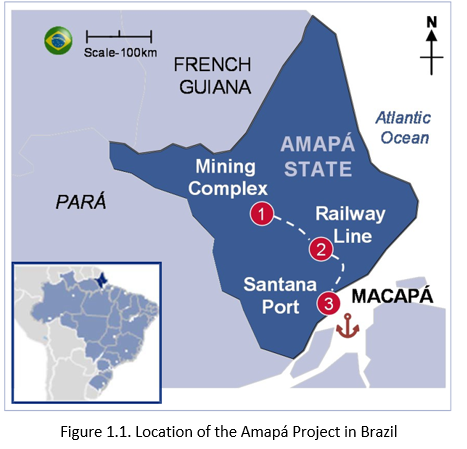

Location

The Amapá Project is in Amapá state, northeast Brazil. Amapá is the second least populous state and the eighteenth largest by area. Most of the Amapá state territory is covered with rainforest, while the remaining areas are covered with savannah and plains. The State capital and largest city is Macapá (pop. circa 500,000), with the similarly sized municipality of Santana (pop. circa 120,000) located just 14 km to the southwest.

The Amapá mine is some 125 km northeast of the state capital Macapá, and the port facility is located on the Amazon River in the municipality of Santana, close to Macapá.

The port site in the municipality of Santana is located 90 km from the mouth of the Amazon River. The nearest populace centre to the Amapá mine is Pedra Branca Do Amapari, some 10 km west, with the larger conurbation of Serra do Navio 18 km to the northwest.

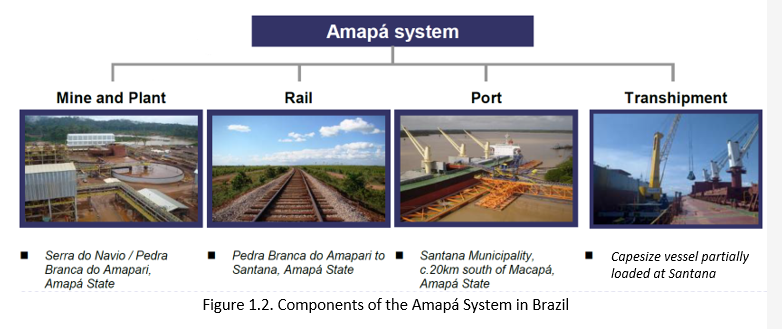

Amapá Project Components

The Amapá Project PFS encompasses four distinct but completely integrated operational components that form part of the study, as illustrated in the figure below.

Amapá Mining Complex

An open-pit iron ore mine with various open pits, an iron ore concentration and beneficiation plant, associated waste rock dumps, and a tailings management facility.

Railway Line

Integrated 194 km railway line connecting Serra do Navio to the port terminal at Santana. The rail passes via Pedra Branca do Amapari (180 km from the port), located 13 km away from the Amapá mine and plant complex by graded road.

Export Port Terminal

An integrated industrial port site, privately-owned and controlled by DEV, is located in Santana. The terminal had the capacity for loading Supramax and Handymax vessels.

Transhipment Solution

A Capesize vessel is partially loaded at the berth in Santana port and topped off in the open ocean, 200 nautical miles from the berth.

Pre-Feasibility Study

The PFS scope covers the existing mine, plant, rail, and port. Capital and operational estimates were developed for refurbishing the facilities to a safe working level. The study investigates all the design and business parameters necessary to operate the Amapá Project, including the railway system and privately owned port for loading vessels with iron ore concentrate. It has also included an upgrade to the existing plant with new equipment and improved efficiency to produce 4.36 Mtpa of Blast Furnace Pellet Feed (“BFPF”) and 0.92 Mtpa of spiral concentrate, a total of 5.28 Mtpa (on a dry basis).

Cost Estimates

The capital costs (“CAPEX”) estimate is based on the layout for all areas of the Project and is supported by mechanical equipment lists and engineering drawings. The costs for these items have been derived from vendor quotes for the equipment and materials or consultant engineering databases. The CAPEX estimate is after tax (any duties and taxes deemed to be recoverable are calculated separately), includes contingency, and excludes escalation. The CAPEX estimate includes all the direct and indirect costs, local taxes and duties and appropriate contingencies for the facilities required to bring the Project into production, as defined by a Pre-Feasibility level engineering study.

As this is a PFS, the cost accuracy is estimated at ± 25% and has a base date of June 2022. Pre-Production capital cost estimates are provided below.

Table 1.2 Pre-Production capital cost estimates

| Description | (US$M) |

| Direct Capex Mining | 2.8 |

| Direct Capex Beneficiation Plant and Mining | 155.1 |

| Direct Capex Rail | 28.5 |

| Direct Capex Port | 113.9 |

| Sub-total Direct Capex | 300.4 |

| Sub-total Indirect Capex | 65.2 |

| Environment and Community Cost | 7.1 |

| Deduct Tax Credit | 25.6 |

| Contingency | 52.1 |

| Pre-Production Capex Cost | 399.1 |

Table 1.3 Deferred, sustaining, and closure capital costs over LOM

| Description | (US$M) |

| Capex Tailings Storage Facility (“TSF”) | 9.8 |

| Capex Rail (2nd Phase) | 20.0 |

| Capex Conveyor Belt | 61.2 |

| Stay in Business | 90.7 |

| Closure Costs | 62.8 |

| Sustaining Capex Cost | 244.5 |

Operating expenditures (“OPEX”) for the Project have been prepared based on the Project physicals, detailed estimates of the consumption of key consumables based on those physicals, and the unit cost of consumables.

The periods considered are annual, and production follows the production plan produced by DEV, based on a yearly output of 4.36 Mtpa of BFPF and 0.92 Mtpa of spiral concentrate, a total of 5.28 Mtpa (on a dry basis).

OPEX comprises physicals, labour, reagents and operating consumables, freight and power costs, mobile equipment, utilities, maintenance and mining contract costs, external contractor costs, environmental, and miscellaneous/other General and Administrative (G&A) expenses. OPEX estimates were prepared or advised by independent consulting engineers. The estimate is supported by engineering, benchmarking, and pricing of key consumables and costs were derived from past production figures and informal quotes from suppliers. The table below illustrates the operating costs developed by discipline during the PFS. The project FOB and CFR average cash cost per tonne of dry product over the LOM is summarised below.

Table 1.4 FOB and CFR average cash cost per tonne of dry product over the LOM

| Cash Cost Per Discipline | US$/dmt |

| Mine | 17.05 |

| TSF | 0.08 |

| Beneficiation Plant, Road / Conveyor Transfer & Rail Loading | 12.43 |

| Rail Freight | 2.43 |

| Port | 1.55 |

| G & A (5% total cost) | 1.99 |

| FOB Cash Costs | 35.53 |

| Marine Logistics | 28.70 |

| CFR Cash Costs | 64.23 |

Project Financial Analysis

A PFS financial model was developed to evaluate the economics of the Project. Summary results from the financial model outputs are presented in tables within this section, including financial analysis. The financial model considers 100% equity funding for the Project, although, in reality, the financing of the Project will be a mix of debt and equity. However, the existing obligations in terms of principal repayment and current interest liabilities payable have been included in the financial model. A summary of the key financial information is presented below.

Table 1.5 Summary of key financial information for the Project.

| Item Over Life of Mine | Unit | 2022 PFS Data |

| Gross revenue | US$M | 9,387 |

| Freight (Maine Logistics) | US$M | (2,350) |

| Net Revenue | US$M | 7,037 |

| Operating costs | US$M | (2,910) |

| Royalties and taxes (excluding income tax) | US$M | (373) |

| EBITDA | US$M | 3,754 |

| EBIT | US$M | 3,315 |

| Net Taxes and Interest | US$M | 355 |

| Net Operating Profit | US$M | 2,960 |

| Initial, Sustaining capital costs & repayments | US$M | 727 |

| Free Cash Flow | US$M | 2,672 |

| Item | Unit | 2022 PFS Data |

| LOM | Years | 16 |

| Discount rate | % | 10 |

| NPV | US$M | 949 |

| IRR | % | 34 |

| Project Payback | Years | 4 |

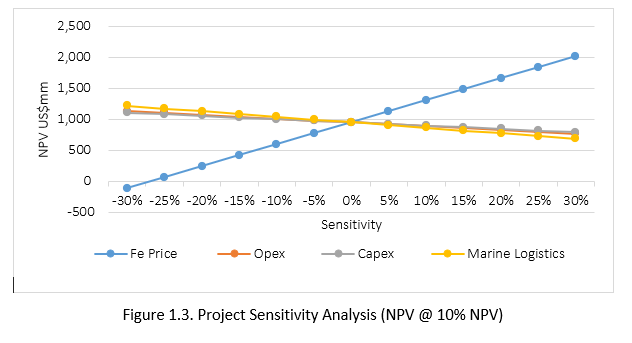

Project Sensitivity Analysis

A sensitivity analysis was performed on key parameters within the financial model to assess the impact of changes on the post-tax NPV of the Project (debt-free). To examine the sensitivity of the Project base case NPV the economic and operational conditions of each cost factor were independently varied within a range of +/- 30%, and discount rates were changed within the 8%-15% range.

Project sensitivity analysis demonstrates that the Amapá Project is most sensitive to a change in iron ore concentrate price, followed by logistics costs (marine shipment charges) and operating costs. It was least sensitive to deviation in CAPEX. The figure below shows the results of the project sensitivity analysis.

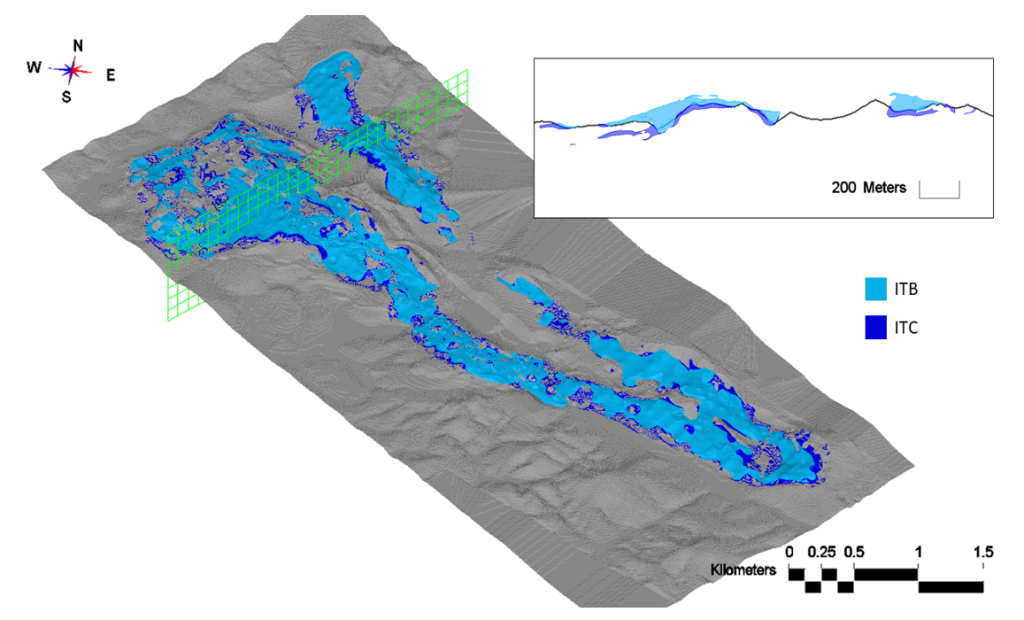

Mineral Resource Statement

The MRE was previously reported on 7 October 2022. The MRE has been reported at a cut-off grade of 25% Fe constrained by a resource open pit and the topography dated April 2014 (grey surface in the figure above), in line with the Reasonable Prospects For Eventual Economic Extraction (RPEEE) principle. The MRE has been estimated, considering a product revenue of US$120/t. The geotechnical parameters, metallurgical recovery and updated mining costs were all provided by DEV.

Table 1.6 Summary of gross and attributable Mineral Resources for the Amapá Iron Ore Project. Attributable tonnage to Cadence is based on a 30% interest in the Project.

| Classification | Tonnage (Mt) | Attributable Tonnage (Mt) | Fe (%) | SiO2 (%) | Al2O3 (%) | P (%) | Mn (%) |

| Measured | 55.33 | 16.60 | 39.26 | 30.40 | 6.54 | 0.161 | 1.03 |

| Indicated | 174.15 | 52.25 | 38.60 | 28.75 | 7.86 | 0.156 | 0.91 |

| Meas. + Ind | 229.48 | 68.84 | 38.76 | 29.15 | 7.54 | 0.157 | 0.94 |

| Inferred | 46.76 | 14.03 | 36.20 | 27.62 | 10.49 | 0.139 | 0.86 |

| TOTAL | 276.24 | 82.87 | 38.33 | 28.89 | 8.04 | 0.154 | 0.93 |

Notes:

(1) The Mineral Resource is considered to have reasonable prospects for eventual economic extraction based on an optimised pit shell

(2) Cut-Off Grade reported within an optimised pit and above a cut-off grade of 25% Fe applied

(3) Tonnages are reported as wet tonnes

(4) Mineral Resources are not reserves until they have demonstrated economic viability based on a Feasibility Study or Pre-Feasibility Study

(5) The Mineral Resource Estimate has an effective date of 31 August 2022

(6) Mineral Resources have been classified in accordance with the Australian Code for Reporting of Exploration Results. Mineral Resources and Ore Reserves (JORC Code 2012)

(7) The attributable tonnes represent the part of the Mineral Resource that will be attributable to Cadence Minerals’ 30% interest in the Project

(8) The operator is DEV

As required per the JORC Code 2012, Table 1 for reporting MREs is available below:

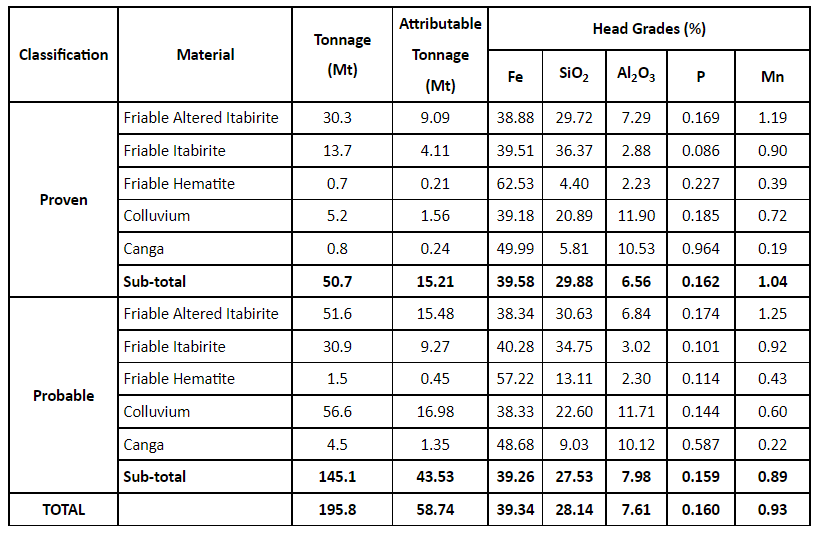

Ore Reserve Statement

The mine engineering and design work for this PFS, including operational logistics, equipment requirements, mining strategy, and Ore Reserve Estimation, have been undertaken by a Brazilian mining consultancy, Prominas Mining Ltd. These works have been conducted at the PFS level and incorporate an Ore Reserve Estimate for open pit mining, which was prepared under the guidelines of the JORC Code (2012).

Under the guidelines of the JORC Code (2012), an ‘Ore Reserve’ is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include the application of considerations to convert Mineral Resources to Mineral Reserves. These considerations include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social, and governmental factors, called ‘Modifying Factors’. Such studies demonstrate that, at the time of reporting, the economic extraction could reasonably be justified.

Prominas has estimated the Ore Reserve for the Amapá Project at 195.8Mt at an average grade of 39.34% Fe, at a cut-off grade of 25% Fe, as presented in the table below.

Notes:

(1) The effective date of the Ore Reserve Estimate is 5 October 2022.

(2) Ore Reserves are reported per the guidelines of the JORC Code (2012).

(3) The Ore Reserve Estimate is reported to a cut-off of 25% Fe.

(4) Ore Reserves were estimated at a selling price of US$120/t (FOB) and include modifying factors related to geotechnical parameters, mining cost, dilution and recovery, process recoveries and costs, G&A, royalties and rehabilitation costs.

(5) A mining dilution factor of 3.0% and a mine recovery of 94% has been estimated and applied for the Ore Reserve Estimate.

(6) Figures have been rounded to an appropriate level of precision for the reporting of Ore Reserves.

(7) Due to rounding, some columns or rows may not compute exactly as shown.

(8) The Ore Reserves are stated as wet (in-situ) tonnes processed at the crusher.

(9) All figures are in metric tonnes.

The Ore Reserve contains only those Mineral Resources which are classified as Measured and Indicated and constrained by an economically and technically mineable engineered pit design, as described previously. The Ore Reserve has also been constrained by the property boundary and considering the position of existing and planned surface infrastructure.

The Competent Person utilised project-specific technical and economic Modifying Factors to estimate the Ore Reserves at Amapá. Sufficient mining and metallurgical work have been completed – and is further reinforced by historical production data – to support the Ore Reserve Estimate.

The Competent Person understands that the Ore Reserve Estimate can be affected by unforeseen metallurgical, environmental, permitting, legal, title, taxation, socio-economic, marketing, or political issues. However, concerning environmental, licensing, legal, title, tax, and marketing considerations, the Competent Person, has relied upon the information presented in the full PFS report. As required per the JORC Code 2012, Table 1, needed for the reporting of Ore Reserves, is available here.

Mine Design

Pit designs and pushbacks were generated using MinePlan® software and adopting preliminary geotechnical, hydrological, cost and density parameters. The designs include benches, berms, and haul roads. The final pit mine design is presented in the figure here.

A LOM production plan was scheduled using the MinePlan® Scheduler Optimiser. The solids used in the mine schedule were based on the final pit design, with an SMU (Selective Mining Unit) of 100 m x 200 m x 4 m. The mining schedule per year is over 13 pits and is shown in the figure here.

Mining

Mining at the Amapá mine will use conventional open pit methods involving drilling, blasting, loading, and hauling ore and waste by a mining contractor. Operations will be conducted based on 365 operating days per year with three 8-hour shifts per day. An allowance has been made for the weather. Ore production is planned at an optimum rate of 12.6 Mtpa. Generally, the total rock mining rate (ore + waste) has been kept below 20 Mtpa. Grade control drilling will be used to delineate the ore zones for excavation as well as low-grade material and waste. Drilling and blasting of ore and waste rock will be required, while overburden materials will be free digging. Ore and waste will be loaded into 100 t capacity off-highway haul trucks to stockpiles, designated waste dumps, or used for construction of the TSF.

Extraction, loading, hauling, and disposal of ore and waste, internal materials handling, mining access opening and maintenance, drainage system operation, and maintenance will all be undertaken by, and the responsibility of, a specialist mining contractor under the management supervision of DEV. For the PFS, DEV obtained a mining cost quote from an experienced Brazilian mining contractor with over 14 years of operational experience in the mining and heavy construction markets.

Processing

Historically the beneficiation plant at the Amapá Project produced four product iron ore concentrates. The development strategy of DEV was to simplify the product stream and focus on higher grade and higher value products, albeit at a lower volume than historical production. The plan is to produce 5.28 Mtpa (dry) of Fe concentrate, consisting of 4.23 Mtpa at 65.4% Fe and 0.92 Mtpa at 62% Fe concentrate. Due to the production history and the metallurgical test work previously completed to achieve the production targets, no further test work was carried out for this PFS.

As far as processing engineering, there were two main work programmes. The first was assessing the current condition of the plant and infrastructure and the work required to refurbish the plant back to its previous state. The second was the flowsheet upgrade and improvements needed to achieve the production mix and targets as proposed within the PFS. ECM Projetos Industriais (“ECM”), who constructed the original Amapá processing plant, was responsible for designing and costing the required process flowsheet modifications and upgrades. ECM conducted an independent analysis of all the data and information available to validate it as the basis for the process design requirements of the PFS Study.

In summary, the process flow sheet consists of an initial crushing, screening, and homogenisation stage. This process produces two streams of crushed ore. The first stream is a +1mm -12mm product fed into the first milling circuit, magnetic separators and then to a desliming circuit before floatation.

The second stream is a -1mm product passed through a spiral circuit to produce a 62% Fe spiral concentrate. Various other flows from the second stream then report either back to the first milling circuit, the second ball mill circuit or the new magnetic separator circuit. The product from the new magnetic separator circuit is sent back to the first milling and then onto a desliming circuit before floatation.

The feed to the deslime circuit consists of the second milling ground product, the first milling circuit magnetic concentrate and the spiral concentrate dewatering screen undersize streams. Desliming occurs via three stages of hydrocyclones. The second and third-stage underflow streams are combined to report to the reverse floatation circuit.

The feed from the desliming circuit is sent to conditioning tanks, where the material is prepared for reverse floatation. The reverse floatation consists of two rougher stages and a final cleaner stage, where the floatation cell tails form the feed for the next step. The final cleaner produces an iron concentrate in which the silica and other impurities have been floated off. This iron concentrate is fed into a concentrate thickener which increases sedimentation. This stream then reports to the filter plant. The filtered concentrate is conveyed to a sampling system and then to the 65.4% Fe BFPF product stockpile. A summary of the process flow sheet can be found here.

Infrastructure

The surface infrastructure from the previous mining and processing operations still exists, including roads, administrative buildings, workshops, and processing buildings. When the mine closed, the mine’s facilities, processing plant, railway and port fell into disrepair. DEV has already begun the rehabilitation of some of the administrative buildings. The intent is to rehabilitate this infrastructure as part of the restart of the Amapá Project, and the costs associated with this were included in the PFS CAPEX.

The Amapá mine’s previous demand was stated as 25 MW; the new power requirement is 30 MW. The existing transmission line, at 69 kV voltage, which interconnects the UHE Coaracy Nunes (Hydroelectric Dam) to Serra do Navio, will not support Amapá mine’s power requirement.

DEV has been in discussion with Companhia de Eletricidade do Amapá (“CEA”) and has been informed that CEA is upgrading the regional transmission lines. CEA intends to construct and upgrade the current transmission line at a voltage of 138 kV from UHE Coaracy Nunes to Pedra Branca do Amapari, then to the plant, connecting to a new 138 kV – 30 MVA substation which DEV will construct. The CEA project timeline for this upgrade is in line with the development timeline of the Amapá Project. Power to the port is provided via connection to the Santana grid provided by CEA and is not expected to require any significant upgrade.

The water supply for the processing plant will come from the accumulated water in the TSF’s water retention ponds. In addition to the TSF return water from normal operations, fresh water will be taken from a local creek and pumped to the TSF. A separate line from the TSF’s return water supply will supply the potable water plant for potable water requirements.

Logistics

As mentioned, DEV owns or has concessions over the key logistics from the mine site to loading vessels at the Port of Santana on the Amazon River. The key logistical components are shown in the figure here.

The access haul road, approximately 13 km in length, is used to access the mine and haul concentrates between the concentrate stockpiles and the railhead at Pedra Branca do Amapari. The option to construct an overland conveyor belt to replace the truck haulage operation is viewed as the best way forward, and this has been included in the process plant upgrade work undertaken by ECM. This work will be completed in the initial two years after start-up.

The rail infrastructure is standard gauge and is 194 km in length, with a distance of 180 km between the railhead and the port. The capital expenditure on the railway will occur over two stages, the latter occurring as deferred CAPEX. Once the second stage of investment is completed, the estimated cargo handling capacity of the railway is estimated to be 6.4 million wet tonnes of ore.

The original port facility was constructed in the 1950s to handle manganese ore and consists of a rail loop, dual bottom-car dumper, central out load conveyor with stacker and reclaimer connected to a floating dock. In March 2013, the port suffered a failure. After the failure, DEV engaged an EPCM contractor to oversee the design and reconstruction of the port facility and associated works. Phase one of the work was completed; however, due to the iron ore price, the construction work stopped shortly after in 2014. Since operations ceased, the port was abandoned and fell into disrepair. The PFS study and CAPEX anticipate the continuation of the works per the EPCM contractor design. The repair of the jack-up rig and the rehabilitation of the port facilities. The figure here shows the planned materials handling and ship loading at the Santana port.

Mineral Title / Permitting

DEV and its subsidiaries own the Amapá Project and its licenses, mining rights and concessions. As the Project was previously operating, it held all the necessary permission to operate. However, since it ceased operations, many have lapsed.

DEV owns four Mining Concessions. The first three concessions are for iron ore, and the last is a gold extraction license. DEV has a joint venture with Mina Tucano Ltda (“Mina Tucano”), which allows Mina Tucano to mine gold and allows DEV to mine iron ore from Mina Tucano’s license. None of the historical mineral resources on license Mina Tucano is included as part of this PFS.

Although DEV owns the Mining Concessions, it does not currently have a Mine Extraction and Processing Permit. To do so, DEV must obtain an Operational License (“LO”) from the state environment authority. Once this has been completed, DEV will apply for Mine Extraction Permit. Since the Project was acquired by its current owners in 2022, DEV has been making the required regulatory filings and embarking on studies and maintenance works to comply with the National Mineral Agency requirements.

Before the suspension of mining, the Project had numerous LOs across the mining, rail, and port operations. These LOs expired between 2013 and 2018. In 2022 DEV began the regularisation of the expired environmental permits. In consultation with the Amapá State Environmental Agency, and the relevant state authorities, DEV has requested that the requirement for an environmental impact study be waived. This request for a waiver was on the basis that the previous LOs were granted on an operation that is substantially the same as is currently planned and remains applicable to future operations. DEV proposes that the company submit an Environmental Control Plan – “PCA” (Plano de Controle Ambiental); and Environmental Control Report – “RCA” (Relatório de Controle Ambiental). DEV has begun its proposed permit pathway for the Project based on the above requirements of a PCA and RCA.

The proposed permit pathway for the Project has both legal and practice precedent and is a reasonable approach, given the Projects status and level of development.

The state owns the railway line and associated land; therefore, for the Project to utilise this, it requires both the LO and a concession agreement with the State of Amapá. The previous operators of the Project were granted this concession in 2006 for 20 years under specific terms and conditions. The reinstatement of this concession to one of DEV’s 100% owned subsidiaries was in December 2019 and was extended to 2046. The concession allows DEV’s 100% owned subsidiary to operate the railway to primarily transport iron ore from the mine to its port in Santana. The State of Amapá owns the surface rights associated with the railway, and under the Railway Concession, DEV has been granted use over these surface rights.

In addition to the LO detailed above, the company’s port is regulated by the Agencia Nacional de Transportes Aquaviários (“ANTAQ”). As a result of the change of ultimate beneficiary of DEV, a change of control request was filed. This change of control was granted in November 2021. As part of the port change of control, ANTAQ has agreed to cease the recommended abrogation of the port concession. DEV owns the surface rights associated with the port.

The principal surface rights applicable to the Project are those above the mining concessions, those associated with the railway from the mine to the port and those associated with the port in Santana, Amapá. The surface rights above the Mining Concessions cover app